The Scale of Disruption Today

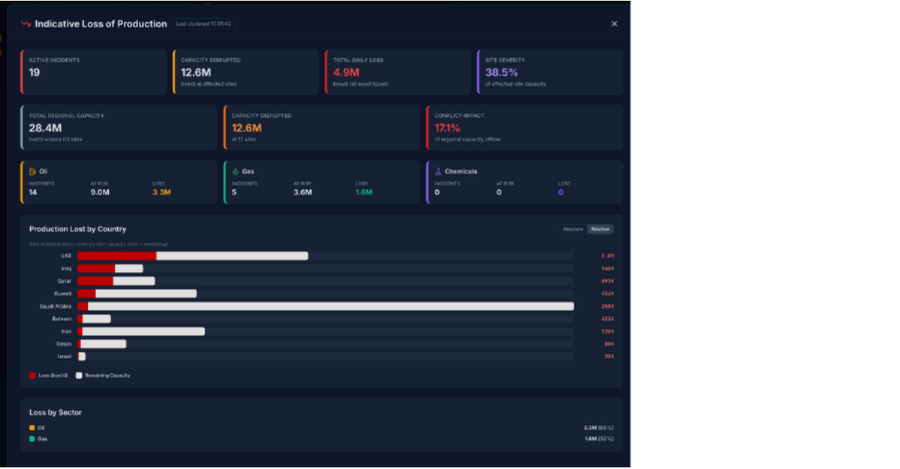

As of 25 March 2026, our Hazard Sentinel platform is tracking 19 confirmed energy incidents across 9 countries, covering oil, gas, and chemical infrastructure from the UAE to Israel. The aggregate picture is stark:

4.9M boe/d — total daily production loss (all asset types)

17.1% — of total regional energy capacity is now offline

12.6M boe/d — capacity disrupted across 17 affected sites

28.4M boe/d — total regional capacity tracked across 63 sites

These are not small numbers. To put them in context: 4.9 million barrels of oil equivalent per day represents more than the entire daily output of Iraq in peacetime. The UAE alone has lost an estimated 2 million boe/d — the result of strikes on Ruwais Refinery (922,000 bpd, fully offline), Fujairah Oil Hub, and Shah Gas Field.

Qatar's Ras Laffan — the world's largest LNG complex, responsible for approximately 17% of global LNG supply — has sustained damage described by QatarEnergy's CEO as requiring three to five years to fully repair. Iraq's Rumaila oilfield, the country's largest at 1.4 million bpd, has been struck by drones. Kuwait's Mina Al-Ahmadi refinery was hit twice in consecutive days. Iran's Kharg Island, through which 90% of Iranian crude exports flow, has been the subject of military strikes on its perimeter.

The Downstream Outlook: Three to Twelve Months

Even under an optimistic scenario in which a ceasefire is reached in the coming weeks, the downstream effects of this disruption are already locked in. Energy markets, supply chains and industrial consumers across Europe and Asia should be planning for the following over the coming year:

LNG supply tightness (0–6 months)

Qatar's LNG trains will not return to full capacity quickly. The damage at Ras Laffan, combined with force majeure declarations on existing contracts, will drive spot LNG prices significantly higher. European buyers who relied on Qatari LNG as a supplement to pipeline gas will face a narrowing window of substitution options. Expect winter 2026/27 gas storage filling to be materially harder and more expensive than last year.

Refined product shortages (1–6 months)

The loss of Ruwais Refinery (UAE), SAMREF at Yanbu (Saudi Arabia), Mina Al-Ahmadi (Kuwait), and Sitra (Bahrain) removes significant regional refining capacity from the market. Diesel, naphtha, and jet fuel supplies to Asian and East African markets sourced from the Gulf will tighten. Industrial consumers dependent on Gulf-origin petrochemical feedstocks — plastics, fertilisers, specialty chemicals — should be reviewing contract exposure now.

Oil price volatility and Hormuz risk (ongoing)

Brent crude has already risen sharply since the conflict began. The Strait of Hormuz remains under pressure — approximately 20% of global oil and LNG transits through this chokepoint. Any further escalation targeting Kharg Island's terminal infrastructure directly, or additional strikes on Saudi Aramco's Eastern Province assets (Ras Tanura, Abqaiq), would be a step-change event for global markets. The risk premium on Gulf crude is now structural rather than temporary.

Energy rationing in the region (3–12 months)

Iran, whose South Pars gas field supplies approximately 80% of domestic gas demand, has sustained significant damage to its primary energy production infrastructure. Domestic gas rationing over the coming winter is a credible scenario. In Kuwait and Bahrain, refinery outages will require product imports to maintain domestic fuel supply — at a time when regional refining capacity is broadly constrained.

Even Resolution Does Not Mean Recovery

It is tempting to assume that a ceasefire resets the clock. It does not. Several of the most significant facilities damaged in this conflict face recovery timelines measured not in weeks but in years:

- Ras Laffan LNG (Qatar): QatarEnergy has confirmed 3–5 years for full repair of damaged LNG trains. The 17% of global LNG supply that has gone offline will not return quickly.

- Ruwais Refinery (UAE): A full-shutdown refinery of 922,000 bpd does not restart overnight. Safe recommissioning of a facility of this complexity typically requires 4–8 weeks under normal conditions — longer following fire and structural damage.

- Rumaila and Majnoon Oilfields (Iraq): Export terminal suspensions and oilfield drone damage have disrupted Iraq's primary revenue source. Rebuilding production confidence and infrastructure integrity takes months.

- South Pars Gas Field (Iran): The backbone of Iranian domestic gas supply has sustained strike damage. Restoring offshore platform capacity in an active conflict environment presents both technical and logistical challenges of the highest order.

For industrial operators globally, this means that supply normalisation — even under a best-case resolution — is a 2027 story, not a 2026 one.

What Industry Can Do Now

At IAMTech, we believe that accurate, timely situational awareness is the foundation of sound decision-making in a crisis. In that spirit, we have made our Middle East Energy Conflict Tracker — powered by our Hazard Sentinel platform — freely available to the global industry with no registration required.

The tracker maps all 19 confirmed incidents in real time, with production loss estimates by country and asset type, displayed across oil, gas and chemical sectors. It is updated continuously as new incidents are confirmed and as production status changes.

Access the public tracker at: hazardsentinel.com — no login, no cost.

The energy disruption we are witnessing is not a spike. It is a shift. The organisations that navigate it best will be those that understood what was happening — and acted on it — earliest.

Ross Coulman | IAMTech

Figures are indicative, based on publicly available sources and IAMTech research. Production loss estimates should be independently verified before use in operational or commercial decision-making. IAMTech accepts no liability for decisions made in reliance on this data.

About the Author

Ross Coulman is the Managing Director of IAMTech, a global leader in industrial asset management and technology solutions. With over 20 years of experience in the sector, Ross has driven IAMTech’s growth from a start-up to a trusted partner for the oil, gas, chemical, and power industries worldwide. Passionate about innovation and sustainability, he champions the use of digital transformation to enhance efficiency, safety, and compliance across complex industrial operations.